best health insurance plan for family India – भारत में परिवार के लिए सबसे अच्छी हेल्थ इंश्योरेंस पॉलिसी कैसे चुनें?

“best health insurance plan for family India” यह phrase सुनने में ज़्यादा marketing‑wala लग सकता है, लेकिन reality में यह बस इतना ही है कि आपको ऐसी policy चुननी है जो आपके परिवार की ज़रूरत, जेब और जोखिम‑स्तर को बेहतर तरीके से बैलेंस करे। इसका मतलब “सबसे सस्ती” या “एक नंबर वाली plan” नहीं है, बल्कि सबसे ज़्यादा suitable और realistic plan ढूँढना है।

1. भारत में family health insurance की basic understanding

भारत के context में:

- healthcare खर्च तेज़ी से बढ़ रहे हैं, खासकर metros और tier‑1/2 cities में।

- वहीं ज़्यादातर families अपनी savings / FD या loan पर निर्भर रहती हैं जब emergency आती है।

- इसीलिए एक अच्छी family health insurance आज लगभग ज़रूरत‑औसत सभी families के लिए financial security का एक core‑piece बन गई है।

तो “best health insurance plan for family India” practical शब्दों में यह है कि:

- आपकी policy आपके शहर‑hospital‑bill level को cover करे,

- claim आसानी से approve हो,

- और long‑term बोझ आपकी जेब पर ज़्यादा न पड़े।

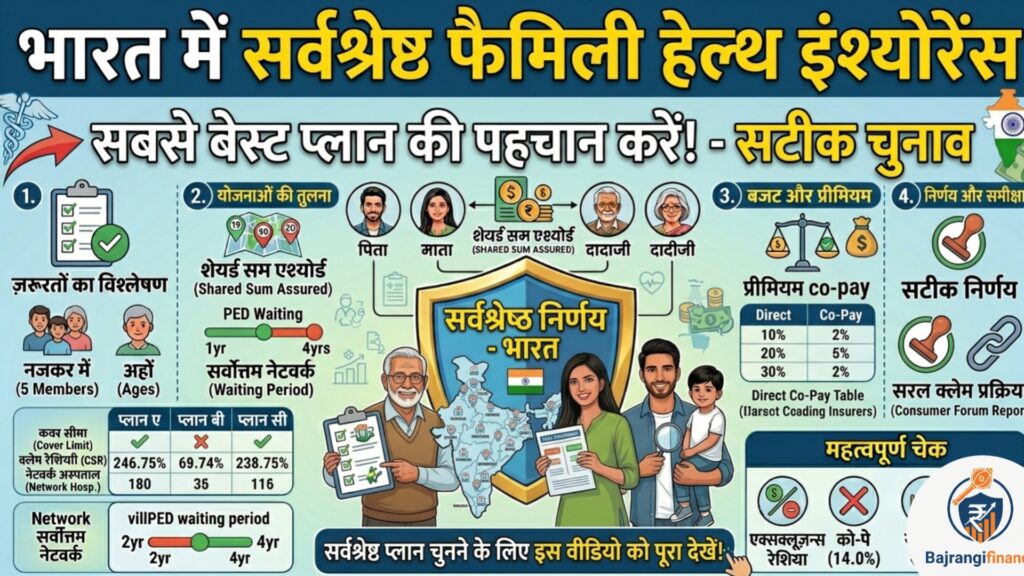

2. family के लिए कौन‑सा type अच्छा माना जाता है?

भारत में लगभग सभी big और reputable insurers family के लिए दो main विकल्प देते हैं:

- Family Floater Plan (सबसे ज़्यादा preferred):

- एक hi sum insured सारे members के लिए common होती है (जैसे ₹10 लाख, ₹15 लाख या उससे ऊपर true/fixed floater वाली).

- ideal रहती है small‑medium families (पति‑पत्नी + 1–2 बच्चे) के लिए।

- premium अक्सर individual plans से cheaper रहती है।

- Individual + Top‑up या Super Top‑up:

- हर member की अलग policy

- और एक common high‑sum top‑up/super top‑up

- इस तरह family की overall cover बहुत high जा सकती है, लेकिन management थोड़ा ज़्यादा complex हो जाता है।

अगर बजट‑friendly और manage‑friendly चाहिए, तो

India में आज family floater वाली policy सबसे common और practical choice मानी जाती है।

3. भारतीय परिवार के लिए realistic sum insured

जब तुम “best health insurance plan for family India” ढूँढ रहे हो तो sum insured ke हिसाब से ये बातें ध्यान में रखो:

- small‑city या छोटी family:

- minimum sum insured = ₹10 लाख true‑floater

- metro / बड़े‑शहर + बुज़ुर्ग included:

- better रहता है ₹15–25 लाख तक की cover रखना।

कम‑से‑कम यह याद रखो:

- ₹5 लाख वाली floater plan आजकल emergency surgeries या complicated treatments में जल्दी खत्म हो सकती है।

- इसलिए “sasti” नहीं, बल्कि “sahi” sum insured चुनना ही वास्तव में best plan बनाता है।

4. India‑specific बातें जो देखनी ज़रूरी हैं

अगर तुम “best health insurance plan for family India” चुनने के लिए criteria तलाश रहे हो, तो इन factors को प्राथमिकता दो:

- Waiting period और pre‑existing rules:

- भारत में ज़्यादातर लोगों को pre‑existing बीमारियाँ (BP, diabetes, thyroid आदि) हैं।

- ऐसे में यह देखना ज़रूरी है कि

- waiting period कितने साल की है,

- और

- policy renew करने के बाद क्या rules change होते हैं।

- copay और deductible:

- बहुत‑सी “cheap‑looking” plans में 10–20% copay या ₹₹5,000–₹10,000 deductible लगाकर premium कम दिखाई जाती है।

- लेकिन बार‑बार hospitalization पर यह तुम्हारी जेब पर extra load डाल सकता है।

- cashless network hospitals:

- जो शहर में तुम रहते हो या जहाँ तुम्हारे रिश्तेदार/relatives रहते हैं, वहाँ के

cashless‑network hospitals आसान होने चाहिए (जैसे अच्छे‑समझदार private hospitals)।

- जो शहर में तुम रहते हो या जहाँ तुम्हारे रिश्तेदार/relatives रहते हैं, वहाँ के

- claim settlement ratio और company reputation:

- कुछ insurers का claim settlement record और white‑paper transparency बेहतर होता है, जो customer‑trust बढ़ाता है।

5. 2–3 policies की comparison – भारत में practical तरीका

तुम “best health insurance plan for family India” चाहते हो, तो इस तरह काम करो:

- कम‑से‑कम 2–3 companies चुनो:

- जैसे:

- A big private insurer (जैसे HDFC ERGO, ICICI Lombard, Bajaj Allianz आदि),

- One PSB‑backed insurer (जैसे SBI General, New India, National Insurance आदि),

- और एक strong‑track‑record वाली private या digital‑focused company (जैसे Digit, Niva Bupa आदि)।

- जैसे:

- उनकी family floater plans की ये बातें लिखो:

- sum insured (true floater या not?),

- premium,

- waiting period,

- copay / deductible,

- cashless network,

- pre‑existing rules.

- फिर वह policy चुनो जो:

- आपकी family‑structure,

- आपकी city / शहर का medical‑cost level,

- और आपकी monthly‑yearly income

इन तीनों को सबसे ज़्यादा logical और आरामदायक तरीके से match कर रही हो।

यही तुम्हारी “best health insurance plan for family India” बन जाएगी –

बिना किसी fake‑title‑chasing वाले marketing‑phrase के।

6. भारतीय परिवारों के लिए एक practical checklist

अगर तुम India में अपने family के लिए अच्छी health‑plan चुन रहे हो, तो इस छोटी सी check‑list से गुज़रो:

- ✓ family‑size और future‑child‑addition को सामने रखकर sum insured देखो।

- ✓ भारत के हिसाब से atleast ₹10 लाख से ऊपर की floater cover रखने पर ज़्यादा consider करो।

- ✓ copay या heavy deductible वाली policy को budget‑cheat की तरह समझकर न चुनो।

- ✓ अपने city और nearby cities के cashless network hospitals की list ज़रूर देखो।

- ✓ pre‑existing disclosures ईमानदारी से करो – यह long‑term में तुम्हारी policy को सुरक्षित बनाएगा।

निष्कर्ष – “best” का मतलब क्या है वास्तव में?

- best health insurance plan for family India का मतलब

“किसी एक magic‑plan” नहीं है,

बल्कि तुम्हारे context, शहर, family‑size और budget के हिसाब से सबसे balanced और realistic plan चुनना है। - थोड़ा सा comparison करके, थोड़ी disciplined premium भरके, और honest‑disclosure follow करके

तुम्हारी family health‑insurance न सिर्फ़ एक document बनेगी, बल्कि तुम्हारे पूरे परिवार के लिए एक real financial safety‑net बन जाएगी।